When it comes to investing, the risk/return tradeoff is a commonly accepted principle. Low risk means sacrificing the potential for growth while high risk offers potential for higher returns, but with greater uncertainty. Accurately identifying your own risk tolerance, the degree of variability in investment returns you’re willing to withstand, is a critical step when selecting your investments. However, it’s equally important to understand how your goals and investment timeline can impact your relationship with risk.

How you think about risk

Is risk a word that conjures images of opportunity and excitement, or a sense of insecurity? For investors, risk tolerance is often closely associated with their goals—specifically the target retirement age and value of retirement accounts. Young investors without a fixed timeline have more flexibility to take risk, while investors closer to retirement tend to make decisions that leave less room for volatility. Time is truly the secret to making investments less risky.

History of risk

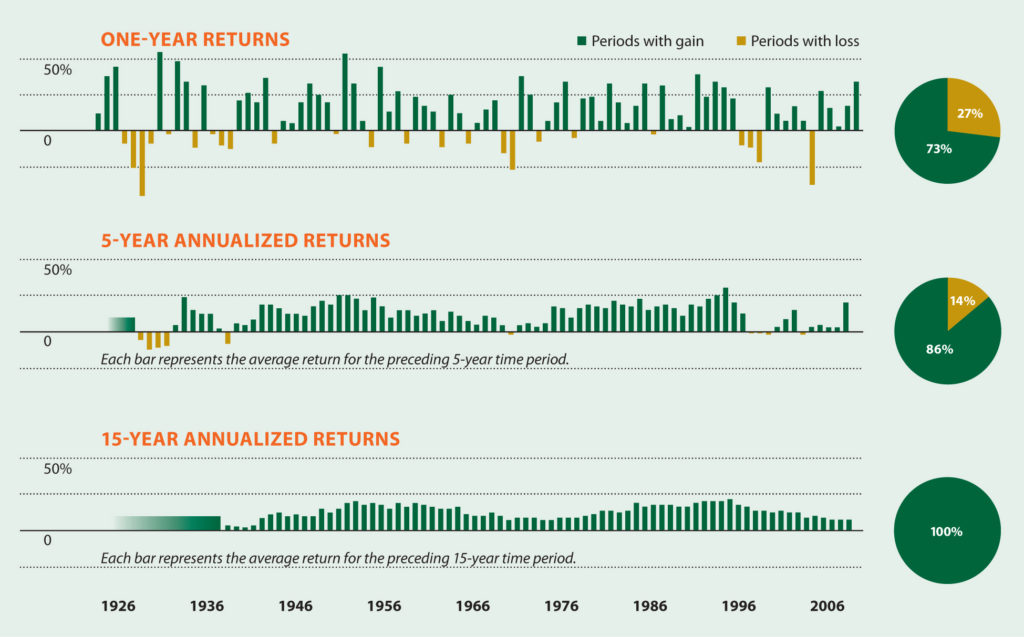

Based on historic market performance, if you invested in the stock market for 1 year, your chance of losing money

would be greater than 1 in 4. The risk drops considerably at five years; but after 15 years that number drops to zero. Simply stated: the longer you keep your money invested, the better your odds of overcoming down markets.

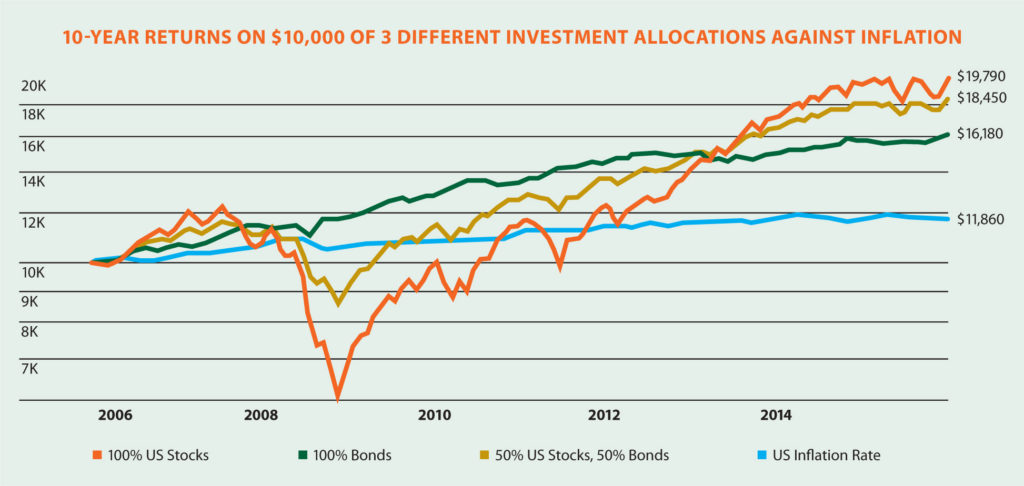

Different types of investments appear at various points

along the risk-reward spectrum.

Managing risk with asset allocation

Managing risk with asset allocation

Different types of investments appear at various points along the risk-reward spectrum. Strategic asset allocation is a way to balance that risk by selecting investments with an investor’s goals, risk tolerance and timeline in mind.

On average, stocks have the highest potential return. Adding bonds tends to reduce the rate of return, but also reduces risk of loss. Once again, the longer your timeline, the greater your chance for gains, even with a higher risk portfolio.

A longer timeline not only helps investors to overcome down markets, it also enables greater benefits from compounding (assuming investments are left alone). Compounding is when an asset generates earnings, which are then reinvested to generate their own earnings; put simply, it’s earnings from previous earnings. Regardless of your goal, the key point to understand is that investment opportunities exist that can help you reach your goal without taking on unnecessary risk.